Apartment Buyers Have a Turkey Problem

Apartment Buyers Have a Turkey Problem

...today’s real estate bros are oblivious to downside scenarios and therefore mortally susceptible to them.

Before Nassim Taleb’s intellectual demise, hastened by the covid panic, he described a real-life phenomenon in concise and informative fashion. To wit, from his book, The Black Swan:

“Consider a turkey that is fed every day. Every single feeding will firm up the bird’s belief that it is the general rule of life to be fed every day by friendly members of the human race ‘looking out for its best interests,’ as a politician would say. On the afternoon of the Wednesday before Thanksgiving, something unexpected will happen to the turkey. It will incur a revision of belief.”

Taleb also provided a chart.

Today’s perma-bullish apartment buyers, who have eschewed objective analysis and placed their faith in endless asset bubbles pumped up by the Fed, are Taleb’s turkeys.

Brimming with confidence reinforced by their ‘lived experience’ over the last several years, these real estate bros are oblivious to downside scenarios and therefore mortally susceptible to them.

Negative Leverage

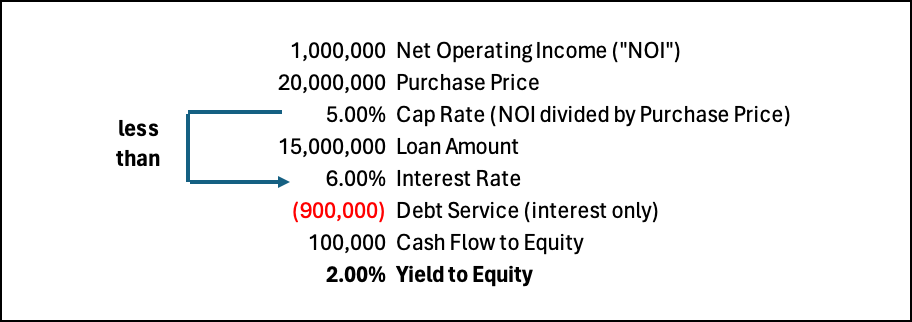

One symptom of the brain fog suffered by apartment buyers is their continued willingness to accept negative leverage, a condition that occurs when the unlevered return, or cap rate, an asset provides is below the cost of debt incurred when acquiring it. The result is illustrated below, and entails a return to investors depressed, rather than boosted, by the use of leverage.

The above example is highly illustrative in that nearly all apartment properties trading in today’s market employ precisely this type and magnitude of negative leverage. Apartment speculators, predictably, justify or ignore this condition using a number of avoidance techniques. They assert that NOI is actually higher than it is. They claim negative leverage is only temporary and NOI will eventually increase to reverse that condition. And they rely on refinancing in the near future because the Fed told them interest rates will be lower soon.

There are significant problems with these reactions, which I won’t enumerate, but this type of thinking is widespread. Per Gresham’s Law, those who don’t think this way have simply exited the market. What’s left are the dregs – those new to investing, with minimal talent and numeracy, drawn to apartments by their relative simplicity and the illusion of easy money fostered by the bubble.

The Average Renter is Tapped Out

Unaffordability of rent is at an all-time high. A recent Harvard study reports that more than half of all renters in the US spend over 30% of their gross income on rent and utilities, with a quarter of all renters spending more than 50%. This metric is known as wallet share, and today’s figures are a clear indication that rents have little room to the upside. Historically, healthy wallet share for a rental market is in the 20% range.

This dynamic puts a damper on the overused investment thesis of raising rents. To do so in an environment where rents are increasing above 30% of wallet share and broad price inflation persists only invites higher delinquency, more evictions, and lower profitability.

Property Taxes and Insurance

Insurance premiums for apartment properties reportedly increased 26% nationwide in 2023. However, those in the industry know this figure is understated. The majority of apartment owners are experiencing like-for-like premium renewal quotes of 50% or more and many are seeing rates double year-over-year. To stem the bleeding, owners are increasing deductibles and shedding coverages where possible. These actions amplify risk of loss over the long-term while saving relatively minimal amounts in the short term.

Likewise, property taxes are jumping at rapid rates. While many states have laws in place limiting assessment increases to 5-10% annually, a transfer of ownership invalidates those limits. Apartment buyers today are looking at massive increases in their property taxes once title changes hands.

Strolling Through the Meadow

Today’s apartment speculator is relatively unskilled, and inexperienced as an investor. Despite severe distress in certain pockets of the apartment sector, a long period of bubble-sustaining machinations by the Fed has done much to limit the damage incurred by these speculators and warp their already limited sense of risk. Relying on artificially low interest rates and a mortgage market subsidized and controlled by the federal government, they’re enthralled by an asset class in which they too can seem like professionals. But like Taleb’s turkeys, their confidence is misplaced. Also like Taleb’s turkeys, once they feel the pain, it’ll be too late.

I wonder how many such investors are aware of potential steep declines in valuations but simply assume they will be bailed out in one way or another. I see this attitude even in seemingly shrewd investors such as those in the Bogleheads forums who assume that when things get "too bad," the politicians will naturally have to step in and save everyone. Do you see similar assumptions in your daily work, or perhaps I am wrong?

Thinking people should always look for the silver lining in every dark cloud. Those struggling to pay exploding rents should move to rural communities with declining populations combined with low rates of crime. Look for a modest fixer-upper on a larger piece of land to allow expansion. Live there modestly, pay cash as much as possible, and enjoy building your castle with your family. Most such communities are thrilled with new faces and have low levels of government meddling. Christian home schoolers have the greatest flexibility as they are not tied to a government building or government school calendar, and will have immediate contact with new friends through the countless Christian home school groups that exist today. Buy, don't rent. Land is cheap in rural communities. Fixer uppers or a pre-fab kit house are really inexpensive. Look at cabin kits or SIPs construction.