The Apartment Market is Uninvestable – Real Time Case Study (Part 2)

The Apartment Market is Uninvestable – Real Time Case Study (Part 2)

...this is not investing. It’s a combination of speculation and something that looks like intent to defraud.

The following outlines the details of a transaction taking place now in the apartment investment market. The transaction is representative of the overall market, therefore broad conclusions can be drawn.

While meant primarily as a presentation of facts, I will be providing context as to how market behavior today has been impacted by the ultra-loose monetary policy of recent history and future expectations of the same.

Lastly, the transaction discussed is based on my direct knowledge of the details, but no confidential or identifying information is provided. Figures used may be rounded or approximated to obscure identifying information, but key concepts are retained.

Sunbelt + Bridge Loan = Trouble

In 2021, three recently built townhome properties in a tertiary West Texas market were acquired by the same buyer. The acquisitions were completed with floating-rate bridge loans. The bridge loans are coming due this year and all three properties are on the market for sale. The overall portfolio comprises 260 units.

While tertiary, the market in which the portfolio is located boasts high population growth, mainly due to the presence of a large university. Nevertheless, those who are familiar with West Texas know that it is a vast area where land is plentiful and often cheap.

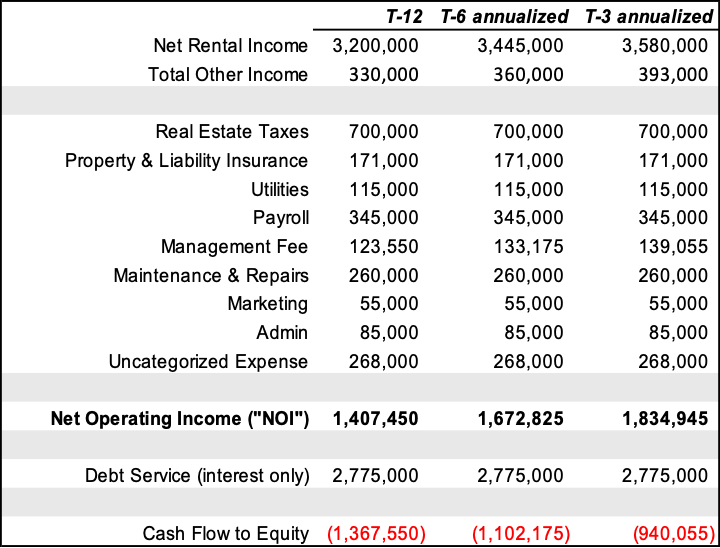

The portfolio produced the following recent performance. Note that “T-3”, “T-6”, and “T-12” refer to trailing 3-month, trailing 6-month, and trailing 12-month revenues, respectively. All expenses are T-12.

Figure 1: Total Portfolio P&L

T-3 figures are highly suspect and easily window-dressed in advance of a sale. Note the incredible 30% increase in NOI from T-12 to T-3, a potential red flag. However, let’s suspend disbelief and use T-3 figures in our analysis.

Even using T-3 figures, this portfolio is plainly distressed, falling short of debt service by over $940,000 annually.

Less experienced analysts might conclude, especially given the age, that the portfolio is only operationally or financially distressed and not physically distressed. This is a mistake. Operational or financial distress leads to cutting corners at the level of staffing and capital expenditure, thus accelerating the physical degradation of the property. This is true with newer properties, and old.

While not shown in the P&L, vacancy issues plague all three properties, with economic vacancy ranging from 12-30%. Aside from poor management, this is due to overbuilding in the market and the fact that recently built properties, like the subject portfolio, have been built at high cost and therefore must charge rents well above market. This is especially true relative to older vintages which were built at far lower cost and can afford much lower rents. Unfortunately for newer properties, tenants are tapped out, and sustainably higher rents are a pipe dream.

A common theme for new properties in overbuilt markets is the need to use excessive rent concessions – financial incentives like free rent that encourage new tenant applications and allow owners to book top-line revenues that appear unimpaired. However, these concessions impact the bottom line and lead to delinquency over time as owners and managers lower credit standards in order to increase occupancy. The subject properties in this case suffer from all of these symptoms.

Online ratings indicate that the properties are not fully staffed, leading to a work order backlog and neglected repairs. This suggests that the P&L, as bad as it is, does not accurately reflect the cost required to run these properties.

Best Case Scenario – Not Good Enough

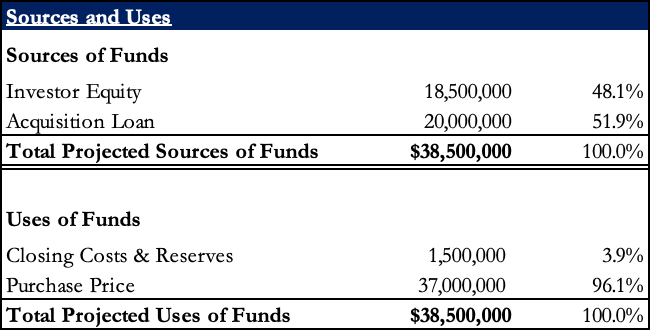

The “whisper price” on the portfolio is $37 million. Assuming costs and reserves of $1.5 million, the total cost to acquire reflects a cap rate of 4.8% on T-3 financials, 4.3% on T-6, and 3.7% on T-12.

Market loan terms for the acquisition demonstrate significant negative leverage, as follows:

Figure 2: Loan Terms

Sources and uses of capital for the transaction are as follows:

Figure 3: Sources and Uses

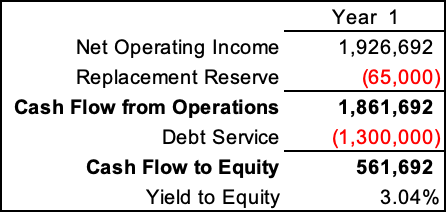

With the information available, we can construct a “Year 1” financial model. For the sake of constructing a “best-case” scenario, we’ll apply a growth factor to T-3 NOI, assume no increases in property taxes, and also assume payroll costs remain the same.

Figure 4: Year 1 Model

Applying no margin of safety to our underwriting pays off with a ‘Year 1’ yield to investors that barely cracks 3%. Keep in mind that this portfolio is located in a tertiary market, is unable to service debt and, absent a sale, will likely be foreclosed by the lender in a matter of months.

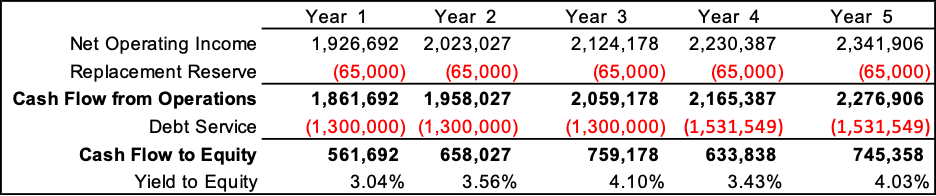

Continuing the analysis with a 5-year model gives us the following:

Figure 5: 5-year Financial Model at 5% Annual NOI Growth

Investors in this acquisition are earning a best-case cash yield of 3.6% over the 5-year hold period – much less than “risk-free” US treasuries pay over the same duration. Reality-based underwriting would no doubt result in cash yields closer to zero.

Who Benefits?

Despite the recent implosions across the apartment market, irresponsible underwriting persists on a wide scale. Investment sponsors are often young and/or inexperienced, familiar only with the speculative environment of the last several years and the ease with which unsophisticated capital has been available. In the above example, prospective sponsors will be forced to make even more optimistic projections than those illustrated in order to make the opportunity attractive to their well heeled but unsophisticated investors. Consideration of downside scenarios or margin of safety is anathema.

Needless to say, this is not investing. It’s a combination of speculation and something that looks like intent to defraud.

The former is a mindset that has been encouraged through successive asset bubbles pumped up by the Federal Reserve and their inability to tolerate downturns in the capital markets.

The latter is a moral hazard involving the transfer of capital from smaller, less sophisticated, investors into the hands of unscrupulous investment sponsors. In recent years, it has become common and fairly easy to source investment capital online through anonymous fundraising channels. A sponsor in need of, for example, $10MM in equity capital, could syndicate such an amount using a feeder fund or online platform designed to aggregate smaller contributions from the general population. For this latter group, the marketing for such opportunities is often irresistible.

On a $25MM acquisition requiring $10MM in equity, the investment sponsor will typically earn a fee of 1.5 – 3.0% of the acquisition price and contribute little or nothing in the way of their own equity. Executed over and over again, the practice can be quite lucrative. Unfortunately for the actual investors, it creates the aforementioned moral hazard. A sponsor who earns significant fees up-front and has little or no skin in the game cares little for whether the investment performs well over time. In their mind, they hold a call option. If the investment succeeds, they get a share in the upside. If it fails, they incur no loss. Only their investors are at risk.

For those wondering why these investment sponsors would risk their reputations in this way, bless your heart.

The Operation Was a Success, But the Patient Died

As demonstrated in the preceding, it takes a certain kind of brain damage to convince oneself and others that fundamentally unattractive investments are feasible. Observing recent history in the apartment market, one would expect a change of approach from sponsors, investors, and other participants. Unfortunately, the easy money of the last several years has lasting effects. Notably, when money is cheap, fools and scoundrels become entrepreneurs. Even now, the apartment syndication industry is working on ways to hone its marketing to attract all manner of liquid but unsophisticated laymen and their capital.

Do you think some/most of the current and future investors in such projects are also under the sway of the bailout regime in the sense that they assume (a) any distress will quickly be remedied by the Fed and (b) the problems in the market were worked out in 2008, so this time is different? As a lay person observing such malinvestment, I want to try to understand what factors, if any, beyond rate manipulation lead people to even consider this (seeming) foolishness.