Multifamily Investment Syndication – A Predictably Unraveling Scheme

Multifamily Investment Syndication – A Predictably Unraveling Scheme

“Only when the tide goes out do you learn who’s been swimming naked.”

In the world of multifamily investment, the “syndicator” is a truly contemptible actor. During the recent bubble in multifamily valuations, syndicators grew fat and happy as a result of incomprehensible amounts of liquidity in the markets looking for a place to invest, regardless of the sponsor’s talent or experience, or the investment’s viability.

As opportunists thriving in a world of malinvestment and easy money, syndicators took advantage of a wealthy but unsophisticated investor pool to acquire properties they intended to quickly flip, riding a wave of speculative asset inflation, earning substantial fees with each closed acquisition, refinance, or sale. It’s a lucrative business while the Fed’s money spigot is on, but eventually that shuts off, and syndicators have nothing substantial (certainly not their reputations) on which to fall back.

Syndicators generally source equity capital for real estate acquisitions from individuals (i.e., retail investors) unknown to them personally. This bottom-feeding process takes place through various sleezy avenues, typically online solicitation, hotel seminars, and the like. This allows syndicators to bypass the difficult work of building relationships based on performance and integrity, instead relying on slick marketing to attract undiscerning speculators.

Syndicators and Bridge Loans – Like Moths to a Flame

During the peak of the multifamily bubble, which took place roughly from mid-2020 to early 2022, syndicators emerged as the preeminent consumers of bridge loans; short-term, floating-rate, high-leverage loans with essentially no underwriting standards that were used to fund roughly 90% of the multifamily acquisition activity during the period.

With no real thresholds to meet, syndicators rushed in to pay more than anyone else for multifamily properties and borrow as much as they could with the aforementioned bridge facilities. Ostensibly the sole investment rationale at play (the actual rationale was earning transaction fees) was the “bigger fool” strategy, essentially a bet that loose monetary policy would never go away, thus fueling continued asset inflation, and allowing the syndicators to “flip” these properties to even bigger fools than themselves.

While they lasted, the bubble conditions enabled these aggressively rent seeking but otherwise dimwitted syndicators to earn significant fees and build up massive assets under management.

Trepp, a provider of loan analytics in the commercial real estate industry, has recently done some interesting work analyzing the portfolios of five such syndicators – Tides Equities, GVA Investments, Nitya Capital, ZMR Capital and Rise48 Equity – and the results are both enlightening and utterly predictable.1

The Chickens Come Home to Roost

Across the five syndicators mentioned, Trepp provides several noteworthy data tables, in the sense that they convey both the utter risk-incompetence from this group that was so emblematic of the multifamily bubble as well as the hopelessness of their current situation given the depth and breadth of the distress illustrated.

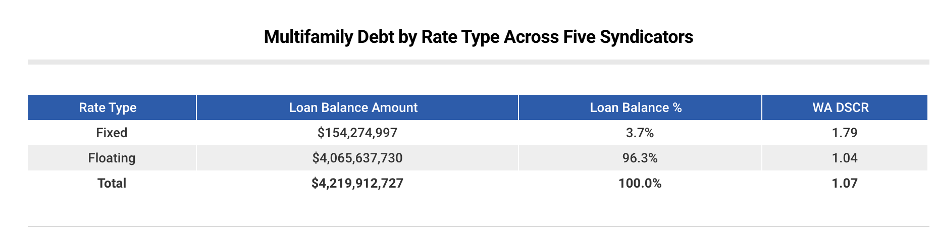

The table below shows the proportion of each type of debt (floating or fixed) employed by these syndicators.

These syndicators were clearly not experienced in risk management, leverage, or basic corporate finance. A full 96.3% of their loan dollars were taken on a floating basis when interest rates were at all-time lows. One of the more interesting corollaries of this observation is that even at all-time low interest rates, fixed rate loans weren’t low enough to provide these investments with positive cash flow! As such, these investors had to take floating rate loans (wherein the initial rate was lower than they could achieve with fixed rates, but with heaps of interest rate risk when benchmark rates eventually rose) just to get the projects to a break-even state on paper.

Looking at the rightmost column, it’s plain to see that these projects are currently generating, at best, barely enough income to service debt. As these are self-reported figures, the more likely case is that sponsors are “adjusting” their reported performance to stay clear of any springing debt service covenants contained in their loan documents. Additional reporting2 has shown DSCR of 0.5 - 0.6x at several of the larger properties owned by these syndicators.

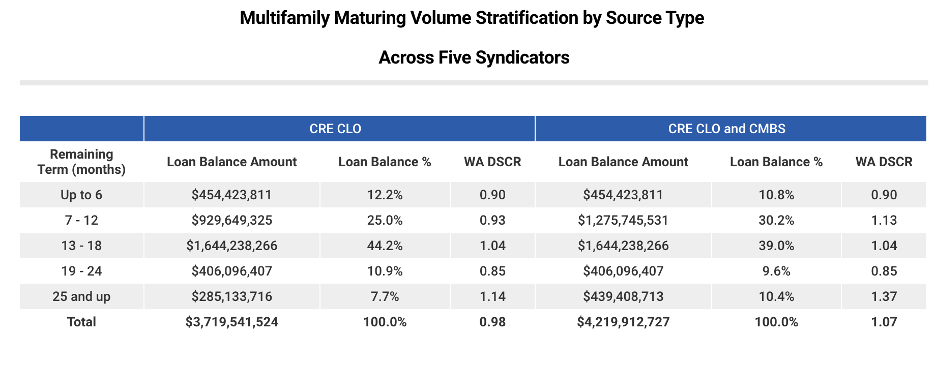

Moving deeper into the Trepp report, one can start to gauge the broader effects this distress might have on the multifamily industry. The table below shows the maturities of the syndicators’ loan book.

What’s apparent here is that roughly 40% of these loans mature in the next 12 months, and 80% in the next 18 months. The drastically lower transaction volume in the multifamily market today is, at least partially, a product of smart money waiting on the sidelines for this distress to play out in the near term, potentially offering compelling value to those who wish to pick at these carcasses.

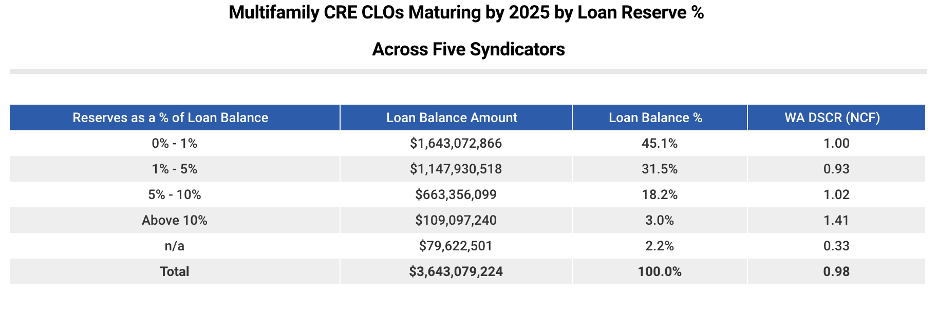

Lastly, Trepp has compiled data related to loan reserves held by these loan portfolios. While current income is clearly distressed in terms of servicing debt, perhaps these syndicators were bright enough to build up cash reserves to carry them through hard times?

They weren’t.

In the multifamily space, healthy reserves would be +/- 10% of loan amount. In the case of these five syndicators, 45% of the loans (by loan balance) have reserves of less than 1% of loan balance, while approximately 87% of the loans have reserves of less than 5%. The “1% - 5%” bucket is not broken down further within that range, but it’s reasonable to assume most of the loans comprising that row are in the lower half of that range, i.e., they have reserves equal to 1-3% of loan amount. Furthermore, lenders are likely to draw down any available reserves in the meantime, to service debt until maturity, meaning most or all of those reserves will be gone by the time maturity rolls around.

Lacking any significant reserves while unable to service debt, fully half of these loans (or nearly $2 billion) will be unsalvageable. Assuming LTVs at acquisition of 75%, that amounts to roughly $650 million in investor equity wiped out by just these five syndicators when the lenders ultimately foreclose the underlying properties.

Summary

As Warren Buffett observed, “Only when the tide goes out do you learn who’s been swimming naked.”

Syndicators and speculators like those mentioned herein were always swimming naked. But they were never meant to be real estate investors in the first place. A tidal wave of easy money, enabled by the Federal Reserve and four consecutive US administrations (from Bush Jr to Biden), lowered the barriers to entry such that no investment acumen whatsoever was necessary in order to solicit and invest other people’s money in highly risky commercial ventures like multifamily acquisition and management. The results should not be surprising, and to some they aren’t.

An additional report on the failure of this particular group of syndicators can be found here: https://therealdeal.com/national/2023/07/06/tides-equities-flew-too-close-to-the-sun-it-wasnt-alone/

See footnote #1