Our Current Asset Bubble, and When It Might End

Our Current Asset Bubble, and When It Might End

The speculative mindset is pro-cyclical in the context of an asset bubble.

William Quinn and John Turner, in their book Boom and Bust, describe the framework of an asset bubble as the confluence of three elements:1

Credit/Money

Marketability, and

Speculation

I’ll discuss how these three factors have impacted the current asset bubble and how one could think about them in determining when a return to sound, non-bubble capital markets might occur.

Credit/Money

Without an expansion of credit, a bubble system has no fuel. An increasing amount of money that’s used to acquire assets provides the basis for any bubble. And in the modern era, the primary driver of credit expansion has been money printing by the central bank – the Federal Reserve in the case of the US.

Mechanically speaking, the Federal Reserve “prints” money and uses it to buy various financial assets from large banks (aka quantitative easing, or “QE”). These assets generally comprise US treasuries, but also corporate bonds, MBS, CMBS and various other instruments, even stocks.

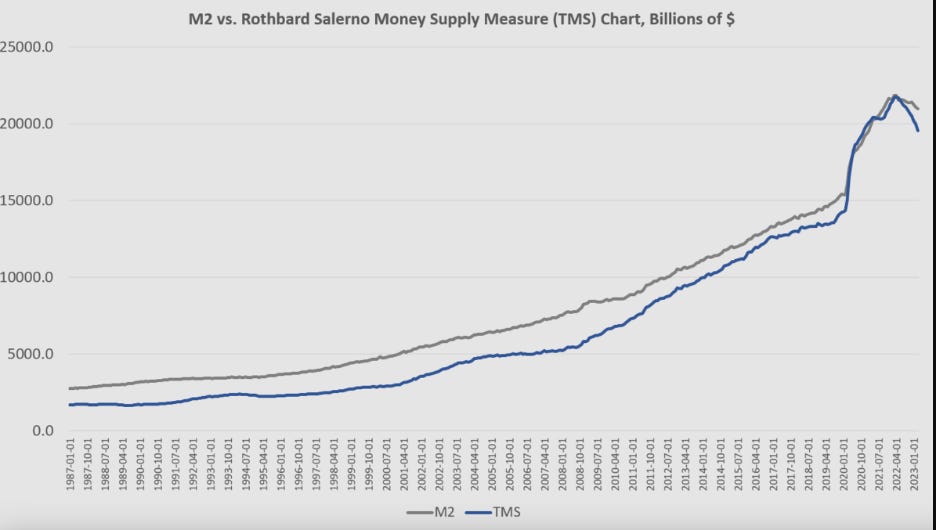

But we should understand the extent of recent increases in the money supply to get a decent grasp of the magnitude of this bubble.

The chart above2 shows two measures of money supply in the US economy. Either can be referenced, they both show essentially the same thing. To wit:

Money supply increasing at a regular pace until 2001, following the bursting of the dot-com bubble, at which point the pace quickened, if only temporarily

A significant uptick in money supply growth following the bursting of the sub-prime credit bubble and the collapse of Lehman Brothers

An astonishing splurge of money printing in the wake of the Covid panic of 2020, followed by our current moderate money supply contraction since early 2022

The party line about QE stimulating the broader economy can be ignored as nonsense, and one can easily discern how creating money from nothing and using it to buy assets could lead to unnatural increases in the prices of those assets, thus enriching the earliest recipients of the printed money - there is little mystery there. What’s remarkable about our current bubble is the magnitude of money printing. Referencing the above chart, the True Money Supply (“TMS”) has quadrupled since 2008, the equivalent of an annual 12% inflation rate during that period!

Our stock of real economic goods certainly hasn’t quadrupled since 2008, so we have significantly more money chasing a relatively small amount of goods. Furthermore, the pace and extent of our recent drop in money supply is dwarfed by the ascent, so several years of continued contraction at this pace would be necessary to arrive at anything like a “normal” money supply relative to the stock of real economic goods.

Marketability

Much has been made of the “gamification” of online stock-trading. Online brokerages have turned it into something resembling a video game. Until recently, before some bad press, the online brokerage scheme ‘Robinhood’ dropped digital confetti on customers after each transaction, as if the act of pressing a button on their mouse or keyboard was cause for celebration.

But the marketability aspect of this bubble is much deeper than cartoonish animations used by online grifters. Consider the recent rise in real estate investment syndication.3

Commercial real estate investment has long been an inaccessible market for most. The analysis required to underwrite such an investment is often complex, the strategies long-term in nature and the legal structure and paperwork extensive. Investors in this field, whether passive participants or sponsors, were well-informed, astute regarding risk, and generally serious about investing their money in such ventures.

Recently, however, pseudo-investors known as syndicators have taken great advantage of the internet and the general climate of speculation to attract investors of a decidedly different quality. Starbucks baristas, greeters at Walmart and pizza delivery boys can now purchase membership interests in an LLC that owns commercial real estate nearly as easily as they can buy goods on Amazon. Syndicators have taken great advantage of the anonymity afforded by online equity-raising to aggressively recruit unsophisticated capital in many thousands of bite-sized chunks without the hassle of relationship-building based on performance.

Even the white-shoe private equity industry has begun offering “quarterly liquidity” to their new army of retail investors, no doubt based on the demands of those same investors that they don’t want to get stuck into long-term illiquid investments, which is exactly what private equity comprises. It hasn’t worked out so well.4

Speculation

Speculation, broadly defined, refers to the practice of buying capital assets with the intention of selling them at a higher price in the near future. No allowance is made for improving the asset by way of expertise or even buying at a price below fair market value (whatever that is) through patience, shrewdness, or other means. Contrary to true investing, which is focused on productivity, frugality and ownership, the practice of speculation is mindless. It involves latching onto an asset that has already appreciated in price and wishing that it will continue to do so. When it does to a sufficient extent, the asset is then sold to the next speculator in line.

The speculative mindset is pro-cyclical in the context of an asset bubble. Speculation contributes to the formation of a bubble, and the bubble breeds more speculation, and so on.

There’s little doubt that the speculative mindset has infected the vast majority of Americans today, helped along by the “marketability” and “credit” problems discussed earlier. Of equal significance to this mindset is the character of our government, a democracy that appears intensely focused on the short-term through the annual plunder of the treasury, such as it is, and the redistribution of wealth from the productive and compliant to the lazy and demanding. We live under a high time preference government, so it’s no wonder that the time preference of the population has increased as well.

Not a Prediction

Predicting the timing of the demise of a bubble is a fool’s game, but given the sheer amount of money still sloshing around the economy (see chart above), the entrenched and embedded speculative mentality of our high time preference population and government, and the internet-powered marketability of further malinvestment and speculation, one can be forgiven for thinking it won’t happen soon.

See https://www.econlib.org/financial-bubbles-and-austrian-business-cycle-theory/ for a summary of this framework and the book in which it’s described. For the website of the book itself, see https://www.boomandbust.co.uk/.

https://mises.org/wire/money-supply-has-plummeted-biggest-drop-great-depression

For a more thorough look at syndication, see here: https://mtsobserver.substack.com/p/multifamily-investment-syndication

https://www.barrons.com/articles/blackstone-stock-price-breit-redemptions-c76143a9